What is the Europe Seaweed Derivatives Market Overview – definition, scope, and significance?

The Europe Seaweed Derivatives Market comprises all commercially produced products extracted or processed from marine macro‑algae, including liquids, powders, and flakes derived from red, brown, and green seaweed species. The market serves a broad spectrum of end‑uses such as food and beverages, agricultural inputs, animal‑feed additives, and pharmaceuticals. Its significance stems from the growing demand for natural, sustainable ingredients that offer functional benefits—like gelling, thickening, and bioactive properties—while supporting the EU’s circular‑economy and marine‑resource stewardship goals.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Seaweed Derivatives Market?

Major drivers include rising consumer preference for clean‑label ingredients, increasing regulatory support for sustainable sourcing, and expanding applications in nutraceuticals and bioplastics. Restraints involve high production costs, limited harvesting infrastructure, and variability in raw‑material quality. Challenges encompass stringent EU food‑safety standards and competition from synthetic alternatives. Opportunities arise from innovations in seaweed farming technologies, valorisation of waste streams, and the emergence of new functional claims that can command premium pricing.

What growth trends are currently influencing the Europe Seaweed Derivatives Market?

Current trends feature a shift toward liquid extracts for beverage fortification, the adoption of seaweed powders as protein‑rich ingredients in plant‑based foods, and the use of flaky hydrocolloids in premium confectionery. Emerging trends include the integration of seaweed bioactives in personalized nutrition and the development of biodegradable packaging films infused with seaweed polymers. Companies are also piloting multi‑species formulations to diversify functional profiles.

How did COVID‑19 impact the Europe Seaweed Derivatives Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains, causing temporary shortages of fresh biomass and delaying new project launches. However, heightened awareness of health and immunity spurred demand for seaweed‑based nutraceuticals, accelerating sales in the food‑and‑beverage segment. Recovery has been swift, with the market returning to pre‑pandemic growth rates by late 2022 and now progressing on a stronger footing, supported by post‑COVID sustainability initiatives.

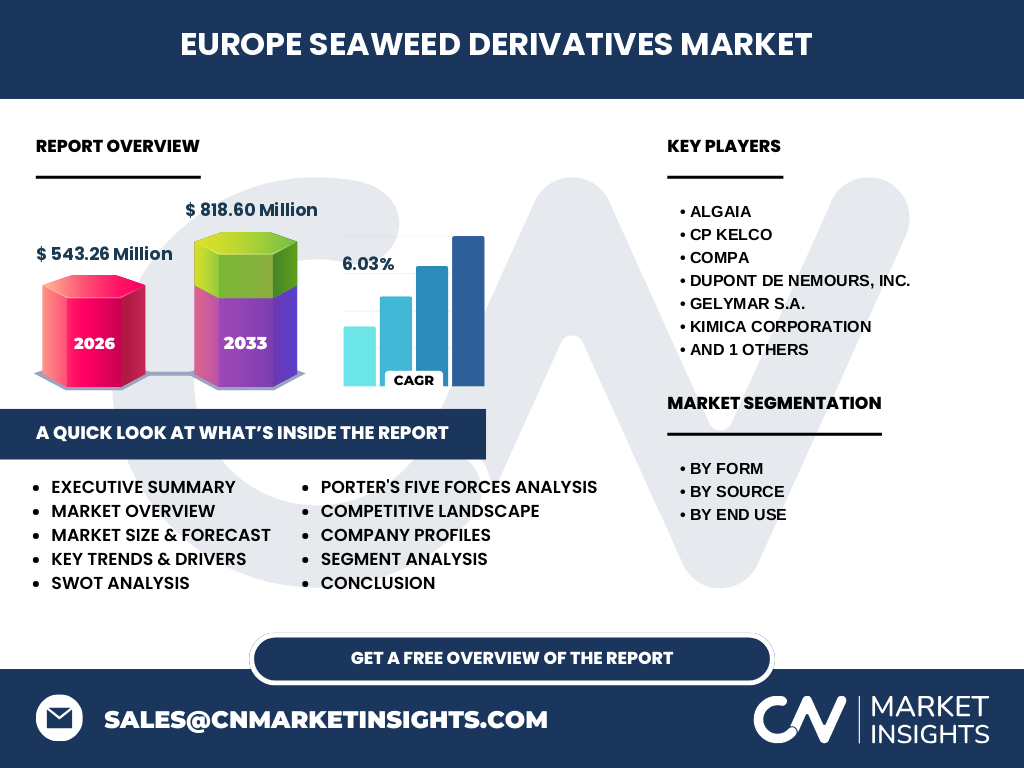

Who are the major competitors and what is the level of market consolidation in the Europe Seaweed Derivatives Market?

The competitive landscape is characterised by a mix of long‑standing marine‑ingredient specialists and large multinational chemical firms. Key players include Algaia, CP Kelco, Compa, DuPont de Nemours, Inc., Gelymar S.A., KIMICA Corporation, and W Hydrocolloids, Inc. While no single entity dominates, strategic partnerships, joint ventures, and selective acquisitions have led to moderate consolidation, enabling firms to expand product portfolios and geographic reach.

What are the high‑level insights presented in the Executive Summary of the Europe Seaweed Derivatives Market?

The Executive Summary highlights a market size of €543.26 million in 2026, projected to reach €818.60 million by 2033, reflecting a CAGR of 6.03 %. Growth is driven by sustainable‑ingredient demand, expanding applications across food, agriculture, animal feed, and pharma, and increasing R&D investments. The summary underscores Europe’s leadership in regulatory frameworks, the importance of innovation in extraction technologies, and the competitive edge offered by diversified seaweed sources.

What are the forecast expectations for the Europe Seaweed Derivatives Market from 2025 to 2032?

Forecasts anticipate a steady upward trajectory, maintaining the 6.03 % CAGR through 2032. The market is expected to expand beyond the €818.60 million mark by 2033, with the strongest growth occurring in the liquid and powder forms due to their versatility in food fortification and nutraceuticals. End‑use segments such as pharmaceuticals and agricultural products are projected to outpace the overall market, driven by increasing functional‑ingredient research.

How is the Europe Seaweed Derivatives Market sized and shared by segmentation?

Segmentation by form divides the market into liquid, powder, and flakes, each catering to distinct application needs—liquids for beverages, powders for protein enrichment, and flakes for texture enhancement. By source, the market is split among red, brown, and green seaweed, offering varied polysaccharide profiles (e.g., agar, carrageenan, alginate). End‑use segmentation captures food and beverages, agricultural products, animal‑feed additives, and pharmaceuticals, reflecting the broad functional spectrum of seaweed derivatives.

What is the global Europe Seaweed Derivatives Market size and share by region?

Within the global context, Europe remains a leading consumer and innovator of seaweed derivatives, accounting for a substantial portion of the €543.26 million market in 2026. While precise regional shares are not disclosed, the continent’s strong regulatory support and sustainability focus position it as a key driver of worldwide demand, complementing growth in Asia‑Pacific and North America.

What does the regional analysis reveal about the Europe Seaweed Derivatives Market?

Regional analysis shows robust performance in Western Europe—particularly France, Spain, and the United Kingdom—where food‑tech startups are integrating seaweed extracts into plant‑based products. Northern Europe, especially the Nordic countries, leads in agricultural‑input adoption, leveraging seaweed powders as bio‑stimulants. Southern Europe benefits from abundant natural coastlines, facilitating local seaweed cultivation and supply‑chain efficiencies.

Which companies lead the Europe Seaweed Derivatives Market and what are their strategic approaches?

Algaia focuses on eco‑friendly extraction processes and strategic partnerships with food manufacturers. CP Kelco leverages its global hydrocolloid expertise to broaden its seaweed portfolio. Compa emphasizes niche applications in cosmetics and pharma. DuPont de Nemours, Inc. integrates seaweed derivatives into its broader specialty‑chemicals suite. Gelymar S.A. concentrates on vertical integration from farming to final product. KIMICA Corporation expands its presence through joint ventures in Europe, while W Hydrocolloids, Inc. targets high‑value niche markets with specialty flakes.

How does Porter’s Five Forces model apply to the Europe Seaweed Derivatives Market?

Threat of new entrants is moderate due to high capital requirements for sustainable farming and processing. Bargaining power of suppliers is limited, as seaweed cultivation can be regionalized, but raw‑material quality variability adds some leverage. Bargaining power of buyers is growing, with large food conglomerates demanding consistent quality and price stability. Threat of substitutes remains low to moderate; synthetic hydrocolloids are alternatives but face consumer resistance. Industry rivalry is moderate, driven by product differentiation and strategic collaborations.

What are the SWOT insights for the Europe Seaweed Derivatives Market?

Strengths: Sustainable sourcing, strong regulatory backing, and diverse functional properties. Weaknesses: High production costs and limited large‑scale farming infrastructure. Opportunities: Innovation in bioprocessing, expansion into pharma and bioplastics, and growth of circular‑economy initiatives. Threats: Climate‑related variability in seaweed yields and competition from established synthetic ingredients.

What does the value chain of the Europe Seaweed Derivatives Market look like?

The value chain starts with seaweed cultivation (wild harvesting or aquaculture), followed by harvesting, washing, and drying. Next, extraction and processing convert raw biomass into liquid extracts, powders, or flakes. Subsequent steps involve formulation, quality testing, and packaging before distribution to food manufacturers, agricultural firms, feed producers, and pharmaceutical companies. Supporting services include R&D, regulatory compliance, and logistics.

What key investment insights can be drawn for the Europe Seaweed Derivatives Market?

Investors should focus on companies with integrated farming‑to‑product capabilities, as vertical integration reduces supply risk. Funding innovative extraction technologies promises higher yields and lower costs. Strategic investments in downstream applications—especially high‑margin pharmaceutical and biodegradable‑packaging segments—are likely to deliver superior returns. Partnerships with food‑tech startups can accelerate market penetration.

What conclusions can be drawn about the Europe Seaweed Derivatives Market?

The market is on a solid growth path, underpinned by sustainability trends, regulatory support, and expanding functional uses. With a projected CAGR of 6.03 % and a market size expected to exceed €818 million by 2033, the Europe Seaweed Derivatives sector offers compelling opportunities for innovators, manufacturers, and investors alike. Continued focus on cost‑effective production and novel applications will be decisive for long‑term success.

What research methodology was employed for this market analysis?

The study combined primary interviews with industry experts, secondary data gathering from reputable databases, company filings, and trade publications. Quantitative data were validated through triangulation, while qualitative insights were synthesized to identify trends and competitive dynamics. Forecasting employed a compound‑annual‑growth model anchored on the provided base‑year figures.

What is the scope of this research and its limitations?

The scope covers the Europe Seaweed Derivatives Market across form, source, and end‑use segments, with a temporal focus from 2025 to 2033. Geographic coverage includes major European economies and highlights global relevance. Limitations stem from the reliance on publicly available data and the absence of proprietary financial disclosures for certain niche players, which may affect granularity of market‑share estimates.

Which key companies are highlighted and what recent developments have they announced?

Algaia unveiled a new low‑temperature extraction line to improve bioactive retention. CP Kelco announced a partnership with a leading plant‑based meat producer to co‑develop seaweed‑based texture agents. Compa launched a carrageenan‑derived wound‑healing gel. DuPont de Nemours, Inc. expanded its seaweed‑polymer portfolio for biodegradable films. Gelymar S.A. secured EU funding for a coastal‑farm expansion project. KIMICA Corporation entered a joint venture with a French biotech firm to explore marine‑derived nutraceuticals. W Hydrocolloids, Inc. introduced a premium flake product targeting gourmet confectionery markets.